1. Cyber insurance — 2023 the coming of age of the European market

While cyberattacks are certainly nothing new (remember for example the WannaCry & NotPetya ransomware attacks in 2017?), cyber insurance products have largely remained an oddity for SMEs (<1% equipment rate in France) & midmarket companies (<10% equipment rate in France) who either didn’t feel they’d ever be impacted or didn’t understand the guarantees they’d be entitled to. So contrary to popular belief, the market for cyber insurance in Europe (UK excluded) is still nascent with a country like France writing total premiums of less than €300m, more than 75% of which coming from coverage for very large companies. And these players put another kind of pressure on the market: they feel that the “premium-guarantees-deductible” triangle just doesn’t work for them and hence are setting up alternative solutions such as captive insurance schemes. While this option doesn’t exist for SMEs, the question remains whether the market can come up with the right products.

Meanwhile, in the US, the market is already much more mature and insurtechs such as Coalition, At-Bay, or Corvus (among others) have earned significant respective market shares over the years convincing all market participants of the robustness of their technology and actuarial models. This offers hope to the burgeoning European ecosystem, where there is a flurry of scaleups to watch out for. These players are tackling cyber risk from different angles (and therefore operating under different business models) and, so far, most have earned the backing of well-known VCs:

Product manufacturers: Cogitanda,

Stoik, Dattak, or

Baobab.

– Have built the actuarial logic and determined their own risk modeling, pricing, guarantees, deductibles, and potential exclusions.

– Partnered with specialized TPAs taking over the claims processing (possibly internalized in the future)

– Usually offer one product, their own

– Focusing on the long tail of smaller SMEs

Wholesale brokerage distribution platforms: Finlex

– Offering brokers a detailed comparison of available insurance products (pricing, insurance limits, deductibles, guarantees, exclusion clauses), which they can then use to sell to their own corporate clients

Brokers: Cyberdirekt,

Superscript

– Distributing the product of established players usually directly to SMEs. Offering digital-only subscription process and First Notification of Loss (FNOL).

Pure tech providers:

– Tools to understand cyber risk looking to improve insurer’s underwriting efficiency (i.e.: onboarding better risk):

Citalid, Bastion

– Cybersecurity tools with different product scopes embedding a pre-defined cyber insurance product:

Cybersmart,

Eye Security, Sagenso

If last year we predicted that new cyber-insurance actors will break into the VC scene (see

EYE security,

Cybersmart, Stoik,

Dattak etc), this year we believe things will get better and larger, attracting more market share, interest, and capital. The cyber insurance market for companies in Europe will keep growing at a fast pace (50%+) under the combined trends of i) increased widespread cyber threats, ii) better product transparency (also thanks to regulatory clarity — see

France’s latest law regarding ransomware reimbursements) and iii) improved education around cyber risk and its prevention.

At the same time, the market will also need to radically improve the transparency of its products & pricing if it wishes to capture an increasing share of companies’ cyber budgets.

2. Lasting turbulence for private, public, crypto market

A recent trend in private markets is that they are opening up to quasi-professional investors and retailers (see Moonfare and Carbon Equity). On the other end, private market investors have also benefited from more open and scalable infrastructures to manage funds and investments (see Odin and Vauban). However, as exit opportunities and up rounds become less visible, everyone, especially the last arrived, will be reminded that private investments don’t always go up and have the peculiarity of being less liquid. Furthermore, as for public markets, flight to quality will temporarily hit the new AUM flows. But despite the turbulence, the underlying trend is here to stay. Technology will democratize private market investing and make it cheaper, faster, and more transparent.

We believe 2023 will be a transition year, where B2B platform can focus on rolling out new products and expanding across jurisdictions in Europe. At the same time, the pace of new funds launch from institutional should remain stable and that means room for tech platforms (e.g. reporting solution like Accelex, AIF back-office solution providers like Fundcraft, and Asset Manager accounting & admin solutions like Lemonedge) will keep thriving and gaining market shares.

-

The bad (public markets)

The public market correction has been far from gentle with fintech and insurtech businesses. Some of the big B2C names have been also trading at a negative EV.

With volatility back on track, fixed-income products more attractive, and consumer spending on the freeze, we think retail-focused neo-broker, investment apps, and EMI neo-banks will have to lower CACs and sustain potential customer withdrawals. On the contrary, those that can “own” customer deposits will be prized by higher interest rates and could leverage on that to attract new customers with short-term remunerated deposits.

We expect B2B public market infrastructure startups (eg LemonMarkets, Wealthkernel, etc) to be impacted as well, especially if their main customers are B2C brokers and investment apps.

We think it is time to start looking at fixed income once again!

-

The ugly (crypto)

2022 has clearly been a challenging year in the Digital Assets space. BTC fell back to 2020 levels, Terra-Luna de-pegged, a number of high-profile companies collapsed (3AC, Celcius, BlockFi..) and the scandal surrounding business practices at FTX is only getting bleaker by the day. Coverage of these events has been massive, from Twitter to main newspapers.

Simulation of a portfolio build in Jan 2021 investing 1k$ each in 5 top 10 tokens at that time

But the spectacular demise of a bad actor such as FTX should not necessarily be seen as a failed promise for the potential of Digital Assets. In fact, we believe the recent events should rather be seen as a catalyst for a refocus of investors towards the core crypto infrastructure, decentralized finance as well as new use cases for DLT (e.g. remittance, cross-border payments, trade finance, insurance).

On the other hand, it is glaring that general trust needs to be restored. Regulators’ and Governments’ involvement is expected (and needed). We believe that crypto Regtech and compliance-minded companies will likely benefit from this crypto winter.

3. B2C in the rear mirror, B2B/B2SME with us in the car

B2C fintech to have a challenging year ahead

Acquiring C consumers as a startup is either an art or pure math. In most cases it resembles the latter: trading euros in CAC for euros in LTV, with the mission to have LTV 3X CAC as a minimum. In the golden era of abundant funds, many B2C startups focused on acquiring customers to gain market share, without focusing on efficiency and disregarding oftentimes monetization. Take N26 as an example: EoY 2021 had 8 million clients and only €180m in revenue, or €22.5 ARPU. The CAC was in the range of 40–60.

As VC funding dries up across the continent, many B2C startups will have to cut costs and find ways to add something to properly monetize their user base that, after being flushed with cash during the pandemic, will now probably look to reduce their spending over 2023.

This will likely lead to fewer B2C fintech/insurtech deals with a broader refocus on B2B models.

B2SME slowly moving into B2B

In the past lustrum, many B2B fintechs have been targeting SMEs (see Pleo, Qonto, Agicap…). Reasons for this are manifold but three stand out: huge market, underserved segment, easier needs = good to approach first. With a colder public market and winds of recession, there is a material risk that the SMEs sector will suffer losses. On the other hand, CAC will probably increase as well with a lesser propensity to spend. To mitigate market these risks, B2SME players could begin addressing their products to larger clients who are generally perceived as more resilient in times of recession.

This said, we believe in the next 12–24 months we will witness to fintech moving up-market and investing to enterprise-proof their products.

4. Climate tech’s: more money at play

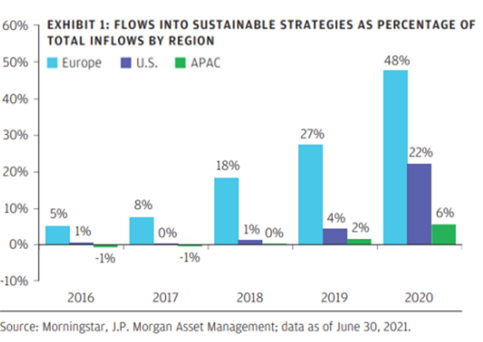

As the world’s population topped 8 billion this year and climate change is an obvious risk for our future, data shows that the EU is the most advanced in terms of ESG awareness, client demand, regulation, and total inflows into ESG-related financial vehicles.

As the demand for them is growing, many Funds are implementing sustainable criteria to design financial products to fit with these evolutions. In fact, the global ESG AUM went from $14tr in 2014 to $39tr in 2021 or a 14% CAGR. MSCI, the leader in ESG data, saw its ESG & climate run rate revenues go from $18m in 2010 to $350m in 2021 or a 31% CAGR. The VC industry will have a central role in fostering climate change and it is already at work.

$100B in new AUM for climate across 132 vehicles — Courtesy of CTVC

We believe 2023 will be a year where also the largest generalist VCs will heavily invest in “climate tech”. Although not all climate tech startups are fintech, the overlap is significant (5–10% of climate deals is also a fintech/insurtech) and the need for tools to measure/reduce risk, account for emissions, rate products, research, and invest is massive. And of course, where there is fintech, there is BlackFin.

A few trends we will support in 2023:

-

B2C neo banking spicing up (Treecard, Onlyone, Helios, GreenGot)

Feature-reach products and proximity to the sustainable mission will be key to attracting customers and emerging as leaders. -

Carbon credit quality enablers and verifiers (BeZero, Sylvera, Carbon Plan, Patch)

As efforts to decarbonize the global economy increase, demand for voluntary carbon credits continues to rise. McKinsey estimates the total market size in 2030 could be between $5 billion and $50 billion. Voluntary carbon credit trading is growing at a rapid speed and so is the underlying quality verification market. Carbon offset democratization will be also a key trend for 2023. Our eyes are out there -

More rationality around carbon accounting

We think carbon accounting will be a huge market, however today we are facing 3 dilemmas: a) a crowded market with low differentiation (we think 2 carbon accounting platforms per country is too much); b) automation is still lacking and requires huge investments or verticalisation; c) methodologies are not always aligned and bear a risk of greenwashing. All this coupled together, raises the need for verification and/or protection tools (like dedicated insurance policies) that will be a trend to follow in the coming years.

5. “Ops I did it again” — The new passion of fintech: Ops teams

In the last 3 months alone I have heard at least 50+ times the word “PaymentOps”. I tried to web-search it and the results were deceiving…self-promoting

articles from Modern Treasury (probably one of the mints of the term) and redirections to “Call of Duty — Black Ops…” 😩 Note: I have tried the same exercise with other Ops-related concepts (e.g. revenue, debt, etc) I have heard through the grapevine. Pretty much the same result if not worse. Then how comes this ended in our predictions? Because, in the past 12–18 months, we have followed many founders wishing to ease the life of “Operation teams” (i.e. any team or role supporting any business operation) with “fintechy” products. We think some of these propositions could realistically give birth to new market segments as Shopify or Saleforce did for storefronts and CRM.

The shared value proposition for Ops platform is to remove non-core operational overhead, reducing time to market and costs. Pretty good for the months/years ahead when operational efficiency is sought back. But it is not only cost reduction, it is as well additional intelligence and insight dashboards for teams and VP/SVP/C-level.

Here is a very high-level map of how we imagine the space:

Payment Ops is, for obvious reasons, the Ops category in everyone’s mouth. We already mentioned the topic in last year’s predictions. We double down this year as we believe B2B payment, in all shapes or form, will be the driving trend of fintech for at least the next 5 years. In the past decade, a lot has been done on the receivable side. Payables will be next. To handle outgoing payments (from issuance to reconciliation), almost any company uses a mix of human touch + banking/treasury management infrastructure and, in certain cases, a home-built product/connectivity layer. A payment Ops platform takes away the pain of dealing with legacy infra as well as of self-building APIs and connectivity layers, giving finance teams super powers and efficiency from day 1. Today tech companies are the natural beachhead for such solutions: no legacy + need to stay lean + need to scale fast BUT have low volumes + low complexity + can churn when growing larger. We think in 2023 many adjacent fintechs (e.g. spend management, CFO-tools, etc) will enter the game of payables and compete to deliver the best and smother experience for SME and Entreprises. Brace yourself as the payables’ war has begun.

Revenue Ops is not something new. It is a topic that dates back 10y at least, however, AI has revamped it big time. The whole concept is around giving S&M teams (+ C-level) collaboration and predictive tools that, by connecting to a number of tools like HubSpot, Google Analytics & co, help them find the best path to deliver revenue targets, support with all the necessary toolset to close a deal and, eventually, help with re-forecasting. A kind of lifeline between the CEO/CFO and the CRO functions. We like a lot the angle, but keep some doubts about the scalability as it appears use cases are not that standardized yet. Anyhow, we believe in 2022 the Revenue Ops category will welcome some new names and bring to life more concrete and bold use cases. We are really looking forward to it!

The “Other Ops” is our catch-all category. We put here other Ops trends we think are worth exploring. One of the hottest is clearly Pricing Ops, where we gathered examples of software platforms that streamline the operations behind pricing a product or service (be it recurring, by consumption/usage, etc). API-economy + automated usage-based pricing software sounds quite a good match. A rather new Ops category is also emerging around debt. Today many fintech run a “balance sheet” business. Handling debt operations is far from easy and require a quite sizeable team. A new breed of actors is blossoming to bring away complexities like setting up SPVs, tracking covenants, monitoring ratios, and so on.

All in all, we believe Ops fintech will be a very exciting category to further deep-dive in the next 12 months.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://www.finextra.com/blogposting/23502/5-fintech–insurtech-predictions-from-a-specialised-vc?utm_medium=rssfinextra&utm_source=finextrablogs