- High-duration US stocks underperformed, Nasdaq 100 on track for worst weekly performance since 6 March 2023.

- US dollar sold off with the USD Dollar Index at risk of breaking below 100.95 key support.

- Asian stock markets are on weak footing despite the current bout of USD weakness.

In his first semi-annual US congressional testimony to the House Financial Services Committee, Federal Reserve Chairman Powell reiterated that the Fed’s current objective is to reduce elevated inflationary pressures to the “traditional” 2% target.

Thus, Powell has implied that the Fed’s mantra is now curbing inflation over negating the possible adverse after-effects on economic growth from tighter credit conditions. In terms of the Fed funds rate trajectory, it’s the same guidance as the latest dot-plot projection released at last week’s FOMC meeting; two more hikes of 25 basis points each before 2023 that bring the median projected terminal Fed funds rate to 5.6% in this current hiking cycle. It’s a “skip” not a “pause” towards higher interest rates for a longer period.

So, it’s almost a “kiss goodbye” for any hopes of an interest rate cut in the second half of 2023 where at the start of Q2, the expectations have been a cut of 75 bps to 100 bps to the Fed funds rate before 2023 ends based on the pricing of 30-day Fed Funds futures (CME FedWatch).

These dovish expectations inferred from the 30-day Fed Funds futures have dwindled in the past four weeks and right now, such bets are almost gone with only a slight chance of 6.4% for a cut during the 13 December 2023 FOMC meeting at this time of the writing.

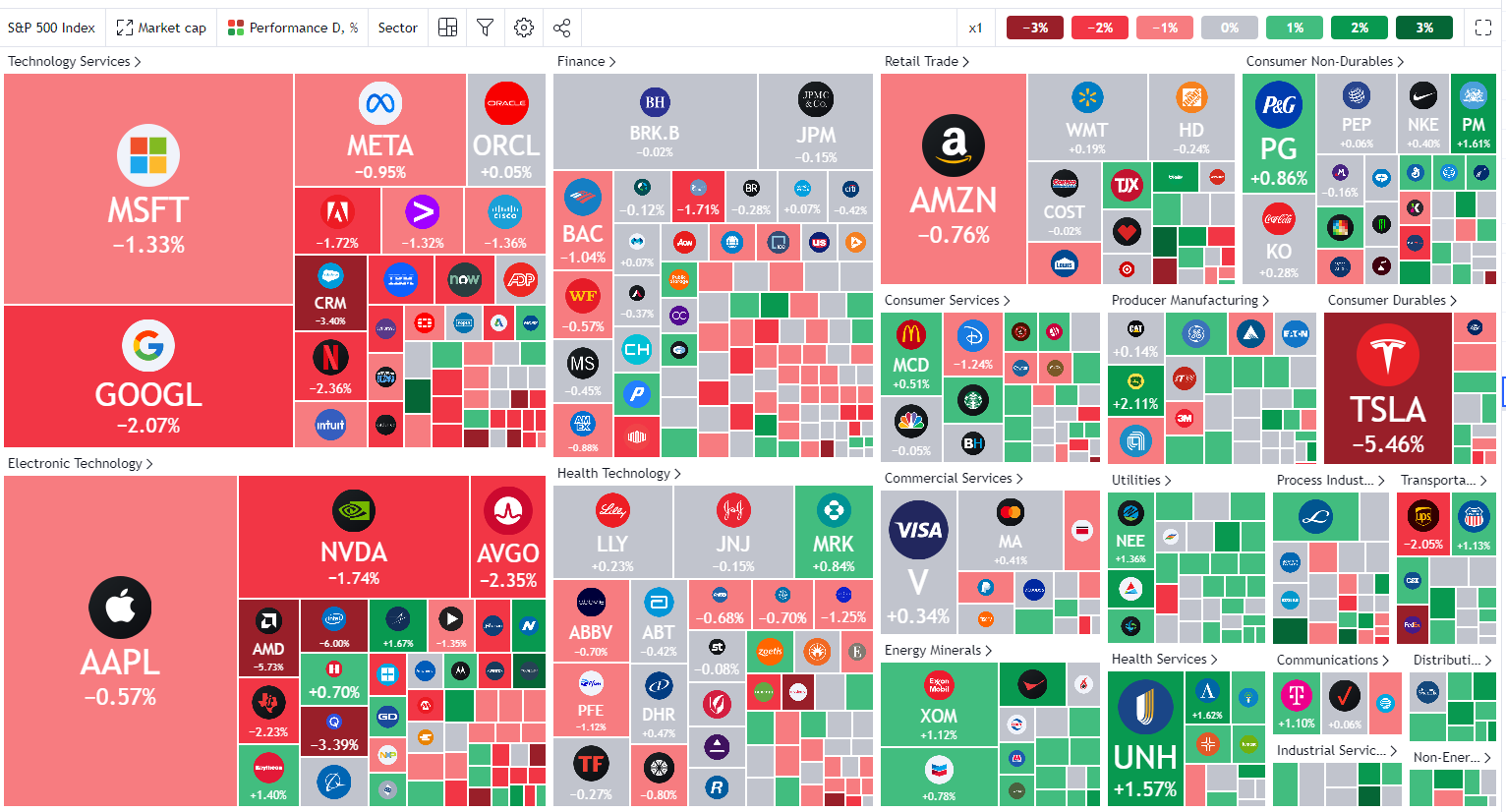

Long-duration risk assets sold off the hardest

Fig 1: S&P 500 component stocks daily heatmap as of 21 Jun 2023 (Source: TradingView, click to enlarge chart)

Growth-oriented risk assets/equities that thrive on a higher degree of operating and financial leverage to boast net profits and do not have stable and or high dividends payouts ratios are classified as “long-duration”.

Because investors tend to benefit primarily from share price appreciation rather than dividends from such growth-oriented long-duration equities and a lower interest rate environment also plays a key contributing factor to add as a potential impetus for share price appreciation.

Since the start of the year, US mega-cap technology heavily concentrated Nasdaq 100 together with the optimism in “Artificial Intelligence” (AI) outperformed in anticipation of several cuts in the Fed funds rate in the second half of 2023.

Right now, it is the reverse that has taken shape, the Nasdaq 100 has declined by -1.44% since the start of this week which translated to its worst intra-weekly return since the week of 6 March 2023. Looks like the “gravitational pull” movement may have begun. For more details, click here to read our previous analysis, “AI FOMO versus economic realities” published on 21 June.

Hawkish Powell is not helping a USD strength revival

Fig 2: US dollar Index medium-term to major trends as of 22 Jun 2023 (Source: TradingView, click to enlarge chart)

In the foreign exchange market, we need to look at things and analyse factors from a relative perspective. Yes, Powell has a hawkish monetary policy guidance coming out from the US, but other key G-20 central banks are as hawkish as well, equally, or more.

Canada’s central bank, BoC, the earliest G-20 central bank to kickstart this current global interest rate hiking cycle has opted to raise interest rate in its recent June meeting to take its overnight interest rate to a 22-year high of 4.75% after a pause in the prior two monetary policy meetings.

The latest Canada’s retail sales data for April that was released earlier this week grew much more than expected; 1.1% month-on-month, recovered from March’s print of -1.5%, and above consensus estimates of 0.2%. Hence, the odds have increased for another hike by BoC in July.

The latest inflationary data from the UK is pointing to an elevated sticky inflation environment where both headline and core inflation for May grew faster than expected; the headline rate at 8.7% year-on-year vs. consensus estimates of 8.4%, and core rate came in at 7.1% year-on-year vs. consensus estimates of 6.8%.

Thus, UK’s central bank, BoE is likely to remain in a hawkish mode after today’s widely expected 25 bps hike to bring its bank rate to 4.75% and the futures market is pricing another five to six more hikes of 25 bps each down the road.

In addition, the latest’s guidance from Eurozone central bank, ECB officials have indicated that it is likely ECB will continue its interest rate hike path trajectory after the upcoming 25 bps hike in July that has been fully priced in. Yesterday, ECB Executive Board member Isabel Schnabel warned that officials could not be complacent about inflation and that raising borrowing costs to a higher level should not be a concern.

Overall, the USD sold off yesterday as the US Dollar Index shed -0.44%, just around 1% away from its current 52-week low of 100.78. From a technical analysis perspective, the US Dollar Index may see weakness in the weeks ahead as this current round of sell-off occurred right at a re-test on the 50-day moving average on Tuesday, 20 June that acted as a resistance at 102.70.

A clear break below the key medium-term support of 100.95 that the US Dollar Index has managed to hold three times since early February 2023 and during the April period where the “de-dollarization” narrative got drummed up may see the continuation of its major downtrend phase to expose the next support at 97.85.

A weaker USD is not helping Asian stock markets

Most of the benchmark Asian stock indices are trading in intraday losses today at this time of the writing with China and Hong Kong markets close for a public holiday.

Even the high-flying Japan’s Nikkei 225 shed -0.9% with Australia’s ASX 200 being the worst performer at -1.6%. In addition, India’s Nifty 50 is showing signs of exhaustion just right below its current all-time high level of 18,887 printed on 1 December 2022 with an intraday loss of -0.3%.

It seems that the higher cost of funding globally is curbing the risk appetite for Asian stock markets despite a weaker USD environment. Perhaps, more clarity on the timing and the size of China’s impending fiscal stimulus measures may rekindle the positive animal spirits.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Latest posts by Kelvin Wong (see all)

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://www.marketpulse.com/forex/powells-higher-for-longer-interest-rates-spook-risk-assets-and-usd/kwong