The trader funding industry and its business model are quite fragile. The Trader Funding Firms (TFFs), often wrongly marketed as Prop Trading Firms, are around for decades. But their popularity exploded in the recent years. Ideally, these firms do not operate like brokerages, but, like any other companies, a level of regulation is still necessary.

In the first part of the ongoing series, I have distinguished between trader funding and prop trading model. Now, in the second part, I am delving deep into the regulatory structure and legality of TFFs.

How Are TFFs Regulated?

Regulation-wise, TFFs are essentially basic LLCs with integrated e-learning components. Unless a firm starts giving investment advice, making controversial claims, or acting as a retail broker without proper licenses (like My Forex Funds did), it’s unlikely to attract regulatory attention.

Broadly TFFs can be classified in about five types:

1. A pure, standalone company (LLC) without any public affiliation, operating under the assumption or claim that the company itself is a proprietary firm managing its own capital (the most common).

2. A limited liability company for evaluations, affiliated with a non-licensed firm that may or may not be proprietary.

3. A limited liability company for evaluations, affiliated with a licensed capital management or prop firm (a less common combination).

4. A limited liability company affiliated with one or several retail FX brokers.

5. Essentially an (usually unlicensed) retail FX broker.

How to Check the Type of TFF?

TFFs often keep their business models and ownerships under wraps. Although many boast their transparency, in reality, they are not. However, there are some ways you can still check some of the business aspects of TFFs.

1. To check if your TFF or affiliated proprietary company may be acting as proprietary, look them up in the LEI (Legal Entity Identifier) registry (lei-identifier.com). An LEI is a reference code used globally to uniquely identify a legal entity engaged in financial transactions. Presence in the LEI registry doesn’t guarantee proprietary status but indicates that the TFF may have accounts at licensed financial firms.

2. Check local registries for information about the company (e.g., State Business registries in the US or Companies House in the UK): when it was created, who owns it, the nature of its business, and even some financial information.

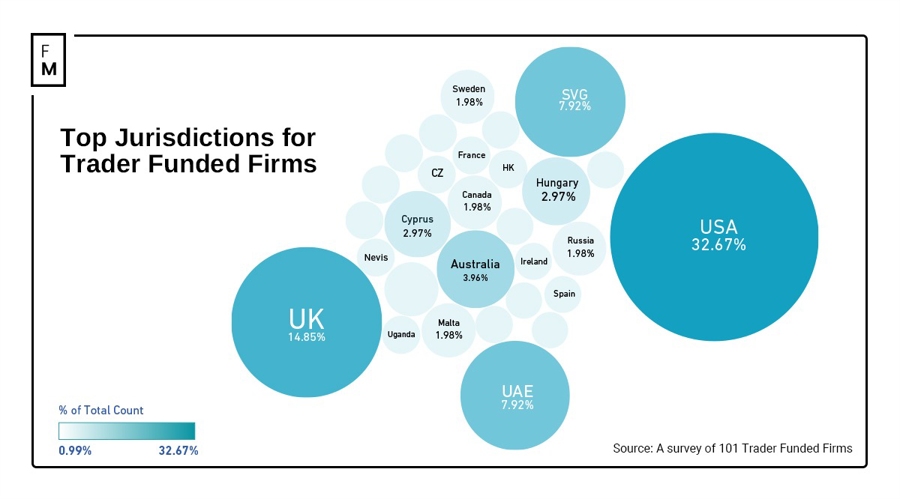

Top Jurisdictions for TFFs

TFF firms are operating globally. Unlike brokers, they do not need a financial services license. However, according to the data from 101 companies, the registration of most of the TFFs are concentrated only in few jurisdictions. The top three such jurisdictions are:

1. the United States of America (Delaware, Wyoming, Florida)

2. St. Vincent and the Grenadines

3. The United Kingdom

Meanwhile the United Arab Emirates and St. Lucia are two emerging jurisdictions for TFFs to set up their shops.

Interestingly, almost every country in Europe has at least 1 trader funding firm incorporated locally. Further, there are quite a few smaller sized firms in India and APAC.

Many are in search of a new prop firm to get funded again and looking for a UAE or a EU based firm to feel “safe”.

It’s not just the jurisdiction that matters. It’s important to know if you are trading a demo account in the name of funded account.

— BF Fx (@BrightFuture_Fx) September 2, 2023

Listed Nature of TFFs Business

Like any other business, TFFs are also have a set nature of businesses. These firms are private and all are indulged into more or less similar activities. Some of the most common business activities of TFFs (at least on paper) are:

1. Recruiting and scouting for traders to trade financial instruments

2. Providing other business support service activities not elsewhere classified

3. Offering eCommerce services for selling various products and services, like courses

4. Providing educational support services to traders

5. Offering other educational technology

Similar Agreements across the Industry

The agreements that traders sign when paying for evaluations are almost identical, with some being word-for-word. After the MFF case, I noticed several TFFs changed their website language to include terms like “simulated” or added “special disclosures” to align with CFTC terminology.

Here are the wordings from one the TFFs: “Unlike an actual performance record, simulated results do not represent actual trading.”

The similarity can be seen on the terms of another TFFs: “Simulated trading programs, in general, are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown. All trades presented for compensation to customers should be considered hypothetical and should not be expected to be replicated in a live trading account. “

“Hypothetical or simulated performance results have certain inherent limitations,” another firm noted. “Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity.”

The wordings runs similar across the industry, as another can be seen from even another TFF’s website: “Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.”

My Funded FX website (live vs archived)

Interestingly, TFFs tend to avoid the term “gaming,” as it could categorize them differently (and even require a license) in some countries, as well as influence their banking and payment accounts.

Common Denominators of TFFs

Apart from the language and agreement, the offerings and services of TFFs are also very similar. Indeed, their core offering of a trader funded business model have to be similar, but the similarities even in the minute details of their offerings are astonishing. Some of these similarities are in the following areas:

1. Professionally designed websites (for about 70%).

2. Well-defined paid “Challenges” with 3+ options based on the desired “funding” amount.

3. A decent amount of educational content (Free or Paid), with clear disclosures that it’s not investment advice.

4. No refunds of evaluation or challenge fees (true for about 90% of firms).

5. Extensive affiliate programs.

In my research, I found many inconsistencies between what’s promised to traders on websites and what’s stated in agreements. Reading the fine print is truly enlightening.

Questionable Practices

Many marketing materials, including the advertisements of TFFs, scream the word “transparency.” However, in reality, there are many questionable practices followed by most of these these TFFs, are least what I have observed. Some of these practices are:

1. Different entities for payments and contracts (e.g., evaluation payment to a UK company, but the contract signed with an HK entity, company branded as a 3rd name).

2. No Disclosures on the website.

3. Claims such as: “We have launched our own in-house proprietary execution broker.”

4. Instant Funding schemes: Pay a $200 evaluation fee for a $10,000 account with 1:100 leverage.

5. Offering higher leverage for higher funding balances (contrary to real-world practices where leverage decreases as buying power increases).

6. Charging retail commissions to DEMO and LIVE funded accounts (proprietary firms surely don’t pay LPs $5 per lot).

7. Dramatically changing trading conditions when an account qualifies for “funded” status (from spreads to execution).

8. Offering Zero Spread.

9. Constantly changing funding account rules.

Honest question. Prop trading firms employ many traders to trade the firms’s money right. Isn’t their edge the risk management practices and processes which are mandated on the traders by the firm?

— 𝑵𝒊𝒔𝒉𝒂𝒏𝒕𝒉🔅 (@typename_nish) April 20, 2021

Some practices may raise eyebrows but have the right to exist, like high-cost trader mentoring (I’ve seen courses for 15k with no-name TikToker) or unrealistic low drawdown requirements and strict trailing stops.

Will TFFs Ever Be Regulated?

I personally think they should be. However, as often happens, a big scandal is needed (I am still following the development of the My Forex Funds case) or heavy lobbying from the top 3-5 industry players. But when would these players ever become interested in essentially adding another expense to their books? This might happen if they start feeling threatened by the increasing number of smaller competitors. Also, considering the current progress of the My Forex Funds case, I highly doubt we will see any major regulatory changes soon.

In the next article, I will cover the technology aspect of TFFs: trading platforms, dashboarding, vendors.

If you would like to read more about jurisdictions/disclosures/best and worst practices of TFFs, leave your email on the waiting list to receive a 50-page long business plan.

Disclosure: The views and opinions expressed in this article are solely those of the author and do not reflect the official policy or position of Advanced Markets.

The trader funding industry and its business model are quite fragile. The Trader Funding Firms (TFFs), often wrongly marketed as Prop Trading Firms, are around for decades. But their popularity exploded in the recent years. Ideally, these firms do not operate like brokerages, but, like any other companies, a level of regulation is still necessary.

In the first part of the ongoing series, I have distinguished between trader funding and prop trading model. Now, in the second part, I am delving deep into the regulatory structure and legality of TFFs.

How Are TFFs Regulated?

Regulation-wise, TFFs are essentially basic LLCs with integrated e-learning components. Unless a firm starts giving investment advice, making controversial claims, or acting as a retail broker without proper licenses (like My Forex Funds did), it’s unlikely to attract regulatory attention.

Broadly TFFs can be classified in about five types:

1. A pure, standalone company (LLC) without any public affiliation, operating under the assumption or claim that the company itself is a proprietary firm managing its own capital (the most common).

2. A limited liability company for evaluations, affiliated with a non-licensed firm that may or may not be proprietary.

3. A limited liability company for evaluations, affiliated with a licensed capital management or prop firm (a less common combination).

4. A limited liability company affiliated with one or several retail FX brokers.

5. Essentially an (usually unlicensed) retail FX broker.

How to Check the Type of TFF?

TFFs often keep their business models and ownerships under wraps. Although many boast their transparency, in reality, they are not. However, there are some ways you can still check some of the business aspects of TFFs.

1. To check if your TFF or affiliated proprietary company may be acting as proprietary, look them up in the LEI (Legal Entity Identifier) registry (lei-identifier.com). An LEI is a reference code used globally to uniquely identify a legal entity engaged in financial transactions. Presence in the LEI registry doesn’t guarantee proprietary status but indicates that the TFF may have accounts at licensed financial firms.

2. Check local registries for information about the company (e.g., State Business registries in the US or Companies House in the UK): when it was created, who owns it, the nature of its business, and even some financial information.

Top Jurisdictions for TFFs

TFF firms are operating globally. Unlike brokers, they do not need a financial services license. However, according to the data from 101 companies, the registration of most of the TFFs are concentrated only in few jurisdictions. The top three such jurisdictions are:

1. the United States of America (Delaware, Wyoming, Florida)

2. St. Vincent and the Grenadines

3. The United Kingdom

Meanwhile the United Arab Emirates and St. Lucia are two emerging jurisdictions for TFFs to set up their shops.

Interestingly, almost every country in Europe has at least 1 trader funding firm incorporated locally. Further, there are quite a few smaller sized firms in India and APAC.

Many are in search of a new prop firm to get funded again and looking for a UAE or a EU based firm to feel “safe”.

It’s not just the jurisdiction that matters. It’s important to know if you are trading a demo account in the name of funded account.

— BF Fx (@BrightFuture_Fx) September 2, 2023

Listed Nature of TFFs Business

Like any other business, TFFs are also have a set nature of businesses. These firms are private and all are indulged into more or less similar activities. Some of the most common business activities of TFFs (at least on paper) are:

1. Recruiting and scouting for traders to trade financial instruments

2. Providing other business support service activities not elsewhere classified

3. Offering eCommerce services for selling various products and services, like courses

4. Providing educational support services to traders

5. Offering other educational technology

Similar Agreements across the Industry

The agreements that traders sign when paying for evaluations are almost identical, with some being word-for-word. After the MFF case, I noticed several TFFs changed their website language to include terms like “simulated” or added “special disclosures” to align with CFTC terminology.

Here are the wordings from one the TFFs: “Unlike an actual performance record, simulated results do not represent actual trading.”

The similarity can be seen on the terms of another TFFs: “Simulated trading programs, in general, are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown. All trades presented for compensation to customers should be considered hypothetical and should not be expected to be replicated in a live trading account. “

“Hypothetical or simulated performance results have certain inherent limitations,” another firm noted. “Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity.”

The wordings runs similar across the industry, as another can be seen from even another TFF’s website: “Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.”

My Funded FX website (live vs archived)

Interestingly, TFFs tend to avoid the term “gaming,” as it could categorize them differently (and even require a license) in some countries, as well as influence their banking and payment accounts.

Common Denominators of TFFs

Apart from the language and agreement, the offerings and services of TFFs are also very similar. Indeed, their core offering of a trader funded business model have to be similar, but the similarities even in the minute details of their offerings are astonishing. Some of these similarities are in the following areas:

1. Professionally designed websites (for about 70%).

2. Well-defined paid “Challenges” with 3+ options based on the desired “funding” amount.

3. A decent amount of educational content (Free or Paid), with clear disclosures that it’s not investment advice.

4. No refunds of evaluation or challenge fees (true for about 90% of firms).

5. Extensive affiliate programs.

In my research, I found many inconsistencies between what’s promised to traders on websites and what’s stated in agreements. Reading the fine print is truly enlightening.

Questionable Practices

Many marketing materials, including the advertisements of TFFs, scream the word “transparency.” However, in reality, there are many questionable practices followed by most of these these TFFs, are least what I have observed. Some of these practices are:

1. Different entities for payments and contracts (e.g., evaluation payment to a UK company, but the contract signed with an HK entity, company branded as a 3rd name).

2. No Disclosures on the website.

3. Claims such as: “We have launched our own in-house proprietary execution broker.”

4. Instant Funding schemes: Pay a $200 evaluation fee for a $10,000 account with 1:100 leverage.

5. Offering higher leverage for higher funding balances (contrary to real-world practices where leverage decreases as buying power increases).

6. Charging retail commissions to DEMO and LIVE funded accounts (proprietary firms surely don’t pay LPs $5 per lot).

7. Dramatically changing trading conditions when an account qualifies for “funded” status (from spreads to execution).

8. Offering Zero Spread.

9. Constantly changing funding account rules.

Honest question. Prop trading firms employ many traders to trade the firms’s money right. Isn’t their edge the risk management practices and processes which are mandated on the traders by the firm?

— 𝑵𝒊𝒔𝒉𝒂𝒏𝒕𝒉🔅 (@typename_nish) April 20, 2021

Some practices may raise eyebrows but have the right to exist, like high-cost trader mentoring (I’ve seen courses for 15k with no-name TikToker) or unrealistic low drawdown requirements and strict trailing stops.

Will TFFs Ever Be Regulated?

I personally think they should be. However, as often happens, a big scandal is needed (I am still following the development of the My Forex Funds case) or heavy lobbying from the top 3-5 industry players. But when would these players ever become interested in essentially adding another expense to their books? This might happen if they start feeling threatened by the increasing number of smaller competitors. Also, considering the current progress of the My Forex Funds case, I highly doubt we will see any major regulatory changes soon.

In the next article, I will cover the technology aspect of TFFs: trading platforms, dashboarding, vendors.

If you would like to read more about jurisdictions/disclosures/best and worst practices of TFFs, leave your email on the waiting list to receive a 50-page long business plan.

Disclosure: The views and opinions expressed in this article are solely those of the author and do not reflect the official policy or position of Advanced Markets.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.financemagnates.com//forex/trader-funded-firms-operate-globally-but-registrations-are-concentrated-in-us-and-uk/