Good morning. Welcome to a monstrously packed Fed week. Chair Jay Powell will face the press on Wednesday, a day after the latest employment cost index, the best-in-class data on labour market conditions, comes out. But don’t sleep on earnings. UPS and Caterpillar, both Tuesday morning, will, hopefully, tell us something useful about a very disorienting business cycle. Email us: [email protected] and [email protected].

More on flab at big tech

Last week we asked whether the biggest US tech companies have gotten flabby. Our argument was that the recent job cut announcements at Amazon, Alphabet, Microsoft, Meta and Salesforce were less about reversing pandemic-era over-hiring (as the companies assert) and more about falling stock prices and keeping restive investors at bay. Big tech share prices are down between a third and two-thirds from their 2021 peaks, and activist investors are pounding their drums menacingly at Salesforce, Meta and Alphabet.

Determining whether the average company has lost focus on costs and returns is not all that complex: you start by benchmarking margins and returns against peers. If the operating margin at toothpaste company A is 12 per cent, and at toothpaste company B it’s 16 per cent, company A has some explaining to do. There may be extenuating factors, but they’d better be demonstrable.

This procedure does not work very well with the very big techs, for two reasons. One, these companies are to a greater or lesser degree unique. There are no very useful comparator companies for Google, Meta or Amazon’s retail business. There are companies that do similar things, but they’re orders of magnitude smaller. For Microsoft and Salesforce, there are other very large enterprise software companies, making comparisons a little easier, but still, business models, markets and delivery technologies differ.

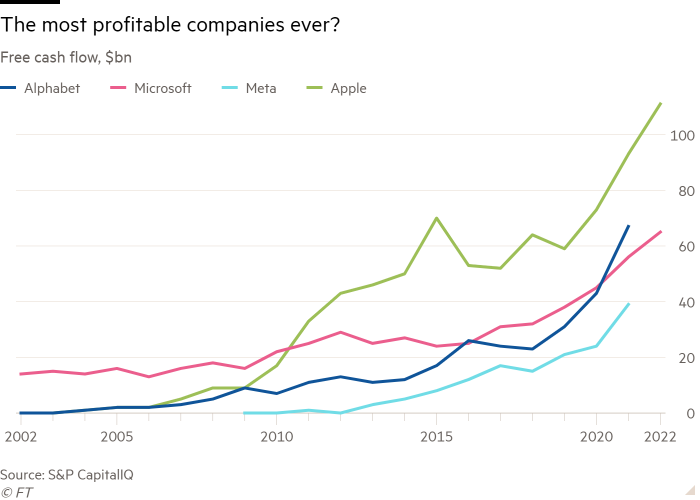

The other problem is that truly enormous software companies are a new phenomenon. There have never been companies of any kind as profitable at massive scale as Microsoft, Google, Meta and (while we’re at it) Apple. They are probably the highest-returning businesses ever (the big oil companies sometimes generate as much profit, but not as consistently). So how profitable could they be if they really focused on profits, instead of building auxiliary businesses and taking moonshots all the time? How can we properly assess their efficiency? We don’t really know; this is all new territory.

With all this in mind, I talked last week to two investors with long experience in these matters. One is a senior executive at Trian Partners, the activist investor currently pushing for change at Disney and Unilever, among other companies. The other is a longtime leader at and investor in tech companies. Neither wanted to be named here.

Trian focuses on the consumer, finance and industrial sectors rather than tech. But my source argued that tech, which was a breed apart in recent years, will now face the same pressures as other companies. “Because the Fed [had] distorted asset prices by making cash free, tech companies did not focus on cash earnings. Now we’re in an environment when cash earnings and dividends matter. Tech was in an environment that incentivised growth. Now all that has changed.”

One key conceptual tool for Trian is the Pareto principle — the idea that 80 per cent of outcomes are determined by 20 per cent of inputs. The point is that the indispensable 20 per cent of products, customers, distribution centres and so forth do not get the attention and resources that they should. Meanwhile, too much energy and care is directed to the mostly irrelevant 80 per cent. One consumer product company, with Trian’s prompting, cut over half of its individual products and revenue fell by less than 2 per cent. Not only does Pareto-pruning make the company more efficient (“complexity is the killer of margin”), but “getting all that gunk out” makes it easier for the company to be more agile and dynamic, and grow more quickly in the future. “Every product needs special materials to make, takes up room in a warehouse, takes up room in someone’s brain.”

The other point the Trian exec emphasised was what he called “matrixing” in companies. This is the tendency to have the revenue-oriented units within a company depend on shared non-revenue functions — manufacture, distribution, advertising and so on. The problem with matrixing is that the costs associated with the shared functions are not attributed to the profit and loss statement of any revenue-generating product teams. The result is that no one is accountable for the costs generated by the shared functions. Furthermore, sharing those functions may not be the most productive way to operate. “You get bloat when you are too matrixed,” he said.

Listening to these points, it occurred to me how little we learned from the big tech companies’ recent job cut announcements. Hearing that, say, Meta is cutting 13 per cent of its workforce teaches me almost nothing, as an investor, unless I know something about where in the company those people were working, and how that unit fits into the larger organisation. It’s just a symbolic number, a general commitment.

The tech investor I spoke to reinforced this point. When he and his team look at a company’s headcount, they consider exactly what new hires are being hired to do (one can commission bespoke research that finds this out by scraping LinkedIn and other public data sources). Are the new hires providing revenue-generating work? Are they, for example, salespeople? Or part of the marzipan layer of middle management?

The hard issue with big tech companies, he said, is that their astonishing profits make them prone to “new age empire-building.” Team leaders will absorb any resources they can, whether they really need them or not, on the assumption that they will need them soon. “If I’m a tech person, I believe in growth — I’ll hire people and figure out how to deploy them later,” the tech investor noted.

There is another layer to the problem. “As a manager, it’s really hard to give margin back.” Once you have delivered a certain level of profitability, your superiors and, more importantly, Wall Street, will complain strenuously if that level is not maintained. So if you are generating high profits, it’s better to spend some of the money adding resources that are not immediately productive. Reporting a quarter or two of terrific margins makes a rod for your own back.

On this analysis, Meta’s mistake, if you want to call it that, was letting Wall Street discover how incredibly profitable its core business was. Once that news was out, lowering margins dramatically to invest in new projects became unacceptable.

This leaves two questions for big tech investors. One: how much unproductive empire-building has there been at big tech? The tech investor points out that Twitter is conducting a “live fire test” on this question, as Elon Musk sacks half or more of the workers there. Second, and perhaps harder: how much of this empire building would you really want to get rid of? Big tech is highly profitable, but it is also highly competitive. Cloud computing, which 15 years ago might have seemed ancillary, is now the most resilient bit of many of the big techs’ businesses. Companies that don’t invest in reinventing themselves, as Microsoft and Amazon have, are taking a big risk.

One good read

Toyota’s warming up to EVs, slowly.

#mailpoet_form_1 .mailpoet_form { }

#mailpoet_form_1 form { margin-bottom: 0; }

#mailpoet_form_1 .mailpoet_column_with_background { padding: 0px; }

#mailpoet_form_1 .wp-block-column:first-child, #mailpoet_form_1 .mailpoet_form_column:first-child { padding: 0 20px; }

#mailpoet_form_1 .mailpoet_form_column:not(:first-child) { margin-left: 0; }

#mailpoet_form_1 h2.mailpoet-heading { margin: 0 0 12px 0; }

#mailpoet_form_1 .mailpoet_paragraph { line-height: 20px; margin-bottom: 20px; }

#mailpoet_form_1 .mailpoet_segment_label, #mailpoet_form_1 .mailpoet_text_label, #mailpoet_form_1 .mailpoet_textarea_label, #mailpoet_form_1 .mailpoet_select_label, #mailpoet_form_1 .mailpoet_radio_label, #mailpoet_form_1 .mailpoet_checkbox_label, #mailpoet_form_1 .mailpoet_list_label, #mailpoet_form_1 .mailpoet_date_label { display: block; font-weight: normal; }

#mailpoet_form_1 .mailpoet_text, #mailpoet_form_1 .mailpoet_textarea, #mailpoet_form_1 .mailpoet_select, #mailpoet_form_1 .mailpoet_date_month, #mailpoet_form_1 .mailpoet_date_day, #mailpoet_form_1 .mailpoet_date_year, #mailpoet_form_1 .mailpoet_date { display: block; }

#mailpoet_form_1 .mailpoet_text, #mailpoet_form_1 .mailpoet_textarea { width: 200px; }

#mailpoet_form_1 .mailpoet_checkbox { }

#mailpoet_form_1 .mailpoet_submit { }

#mailpoet_form_1 .mailpoet_divider { }

#mailpoet_form_1 .mailpoet_message { }

#mailpoet_form_1 .mailpoet_form_loading { width: 30px; text-align: center; line-height: normal; }

#mailpoet_form_1 .mailpoet_form_loading > span { width: 5px; height: 5px; background-color: #5b5b5b; }#mailpoet_form_1{border-radius: 3px;background: #27282e;color: #ffffff;text-align: left;}#mailpoet_form_1 form.mailpoet_form {padding: 0px;}#mailpoet_form_1{width: 100%;}#mailpoet_form_1 .mailpoet_message {margin: 0; padding: 0 20px;}

#mailpoet_form_1 .mailpoet_validate_success {color: #00d084}

#mailpoet_form_1 input.parsley-success {color: #00d084}

#mailpoet_form_1 select.parsley-success {color: #00d084}

#mailpoet_form_1 textarea.parsley-success {color: #00d084}

#mailpoet_form_1 .mailpoet_validate_error {color: #cf2e2e}

#mailpoet_form_1 input.parsley-error {color: #cf2e2e}

#mailpoet_form_1 select.parsley-error {color: #cf2e2e}

#mailpoet_form_1 textarea.textarea.parsley-error {color: #cf2e2e}

#mailpoet_form_1 .parsley-errors-list {color: #cf2e2e}

#mailpoet_form_1 .parsley-required {color: #cf2e2e}

#mailpoet_form_1 .parsley-custom-error-message {color: #cf2e2e}

#mailpoet_form_1 .mailpoet_paragraph.last {margin-bottom: 0} @media (max-width: 500px) {#mailpoet_form_1 {background: #27282e;}} @media (min-width: 500px) {#mailpoet_form_1 .last .mailpoet_paragraph:last-child {margin-bottom: 0}} @media (max-width: 500px) {#mailpoet_form_1 .mailpoet_form_column:last-child .mailpoet_paragraph:last-child {margin-bottom: 0}}

Slimming down Big Tech Republished from Source https://www.ft.com/content/5f96a9f3-e410-4213-9f51-f5f7aba4fd8a via https://www.ft.com/companies/technology?format=rss

<!–

–>

<!–

–>

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://blockchainconsultants.io/slimming-down-big-tech/?utm_source=rss&utm_medium=rss&utm_campaign=slimming-down-big-tech