Banks in Asia-Pacific (APAC) are diversifying their offerings and embracing innovative digital strategies including super-app platforms, financial marketplaces and banking-as-a-service (BaaS) models.

By 2030, these business models and digital offerings will contribute over 40% of banking revenue, representing some of the industry’s biggest growth opportunities for the sector, a new report by Twimbit, a Singaporean research and advisory firm, says.

The paper, titled “APAC banks pursue growth with digital adjacencies”, explores the state of digital innovation in the region’s banking industry, identifying the key trends arising in the sector and delving into the biggest growth opportunities for incumbents.

According to the report, APAC banks are adopting varied digital strategies to remain competitive in a rapidly evolving landscape, with five approaches and offerings emerging as the most prominent growth strategies.

Source: twimbit analysis

Banking-as-a-service (BaaS)

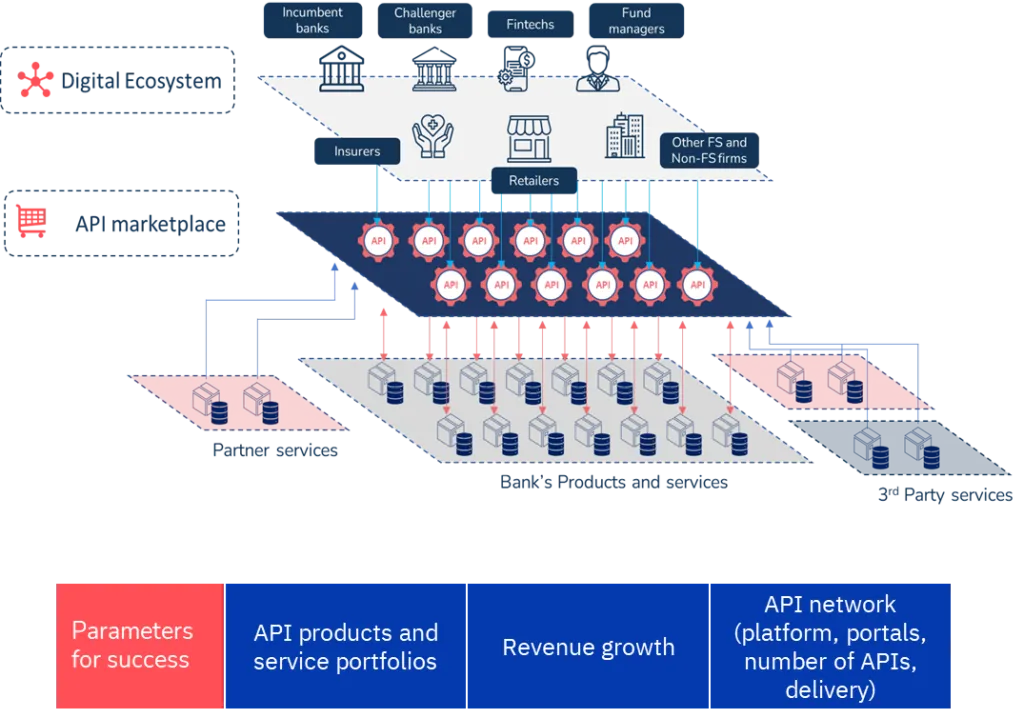

The first trend outlined in the report is BaaS, a business model which involves the provision of banking products to non-bank third parties through application programming interfaces (APIs). This strategy provides incumbents with the opportunity to become providers of white label and co-branded products and services, introducing new revenue streams while also allowing them to significantly reduce the cost to serve and the cost of customer acquisition.

Indian bank and financial services company ICICI Bank is highlighted as one of the top BaaS providers in APAC. The bank boasts a suite of more than 600 banking APIs that are used in various industries including e-commerce, travel, real estate and fintech. The strategy has allowed it to see its non-interest income and total deposits increase by 12.88% and 10.9%, respectively, year-on-year (YoY) in fiscal year 2023.

Source: twimbit analysis

The super-app strategy

The second major growth opportunity outlined in the report is the super-app strategy. This approach consists in developing a digital platform that integrates multiple services and which enables users to access a range of products without leaving the app, leading to higher user engagement and retention. Like BaaS, super-app platforms allow banks to save on costs associated with customer acquisition and operation, leading to improved profitability.

India’s Paytm is one example of a successful super-app platform in APAC. The digital payment and financial services company, which counts more than 100 million active customers and 37 million merchants, offers a variety of services including digital payments, a digital wallet, mobile recharges, an e-commerce platform, bill payments and travel bookings. It leverages the large amount of payment data it collects from customers to offer personalized recommendations and introduce relevant products that meet end-users’ needs.

In Southeast Asia, the super-app market is currently worth US$4 billion in revenue, with a growth projection to be US$23 billion by 2025, the Twimbit paper says. This growth will be driven by surging e-commerce activity and a booming regional digital economy. By 2025, 65% of APAC gross domestic product (GDP) is expected to be digitized, reaching US$1.5 trillion in customer spending. Meanwhile, the e-commerce market is forecast to grow at a compound annual growth rate (CAGR) of 10% between 2024 and 2029, and is set to reach US$6.76 trillion by then.

Buy now, pay later (BNPL) arrangements

Buy now, pay later (BNPL) is another growth opportunity for APAC banks highlighted in the report. BNPL arrangements, which refer to a type of short-term financing that allows consumers to make purchases and pay for them over time, help banks improve customer retention and acquisition, increase transaction volumes, and strengthen their relationships with merchants.

Top BNPL providers in APAC include Atome, a subsidiary of Singaporean tech company Advance Intelligence Group which boasts more than 40 million users across its ecosystem and which has reached a gross merchandise value (GMV) of US$2.4 billion through over 50 million transactions since its inception. Atome provides an array of products that range from BNPL and payment solutions, to loyalty programs and merchant services.

According to market researcher PayNXT360, BNPL payments in APAC are expected to grow by 17.3% on an annual basis to reach US$232.5 billion in 2024. BNPL payment adoption is set to rise at a CAGR of 12.3% between 2024 and 2029, with BNPL GMV forecasted to increase from US$198.2 billion in 2023 to reach US$414.5 billion by 2029.

Banking marketplaces and embedded finance

Another digital trend outlined in the Twimbit paper is banking marketplaces and embedded finance. In APAC, banks are providing financial marketplaces to drive customer trust and loyalty. They are also leveraging APIs to connect with third-party service providers, enabling them to offer a diverse range of products and services within their marketplace.

According to Twimbit, nearly 60% of banks embedded financial services in third-party marketplaces in 2023. Between 2022 and 2029, APAC’s embedded finance industry is projected to grow at a CAGR of 24.4%, reaching a total revenue size of US$358 billion by then.

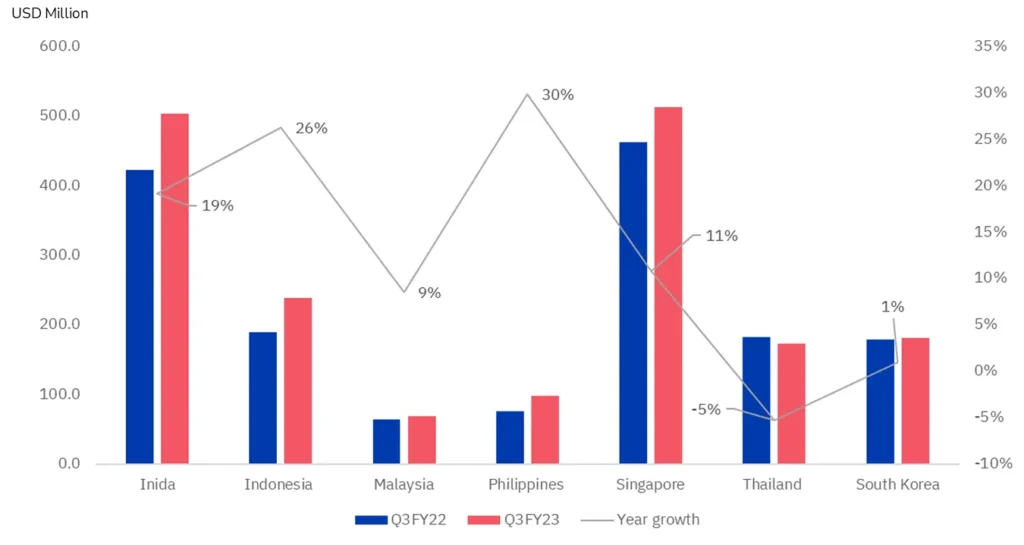

Singaporean bank DBS is one of the region’s most prominent financial marketplace providers, a strategy that has helped it grow its non-interest income by 11% in Q3 fiscal year 2023. Its DBS marketplace lets users buy or rent property, book flights or hotels, switch their electricity supplier, and more, effectively reimagining customer journeys, enhancing relationships, and helping the bank differentiate from competitors in an ever-evolving competitive environment.

Data monetization

Finally, the fifth and last trend outlined in the report is data monetization. Banks are custodians of massive amounts of customer data, which they can leverage to generate additional revenue streams. These data can be utilized to generate insights on customer behavior and build tailored value propositions, enhancing customer engagement and potentially increasing sales of various financial products and services. Banks can also aggregate and anonymize customer data to create valuable insights for third-party companies. These insights can be sold to retailers, market research firms, or other businesses interested in understanding consumer behavior and market trends.

Across APAC but also the broader global landscape, banking incumbents are facing trends and challenges that are compelling them to innovate and adopt digital strategies. First, the report notes that there is mounting pressure to maintain operational sustainability, lower the cost to serve, and explore growth opportunities with non-interest fee-based income. It also notes that the competitive landscape is changing rapidly with the rise of fintech companies and tech giants prompting incumbents to ramp up their digital efforts.

This trend is evidenced by results of a new research paper by the International Monetary Fund (IMF) which found that the rise of fintech is posing a threat to traditional financial institutions. Specifically, the findings reveal that as fintech transaction volumes increase, there is a corresponding negative impact on banks’ profitability, hinting at the fact that fintech companies are eroding the market share of traditional banks.

Featured image credit: freepik

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/87030/digital-transformation/digital-offerings-like-baas-to-contribute-over-40-of-apac-banking-revenue-by-2030/