Introduction

In recent years, it has become easier than ever to move businesses and money into the global economy. This has prompted banks and fintech companies to invest in more efficient technologies for cross-border payments.

In the past, such payments were slow, complex, inefficient, costly, and time-consuming, involving multiple banks with unclear fees and complicated tax rules. However, the banking industry has undergone significant changes. It is now shifting towards digitized solutions that offer cheaper, 24/7 availability, near-instantaneous transfers, and greater transparency.

According to

Juniper Research, global spending on B2B cross-border payments is expected to surpass $40 trillion this year, with a significant portion driven by the growing popularity of e-commerce marketplaces.

Additionally, there is a growing demand for high-quality and convenient financial services, with entrepreneurs, SMEs, and corporations expecting instant transfers regardless of time zone or location. Financial institutions are striving to develop solutions that facilitate international business operations.

What Are Cross-Border Payments & How Do They Work?

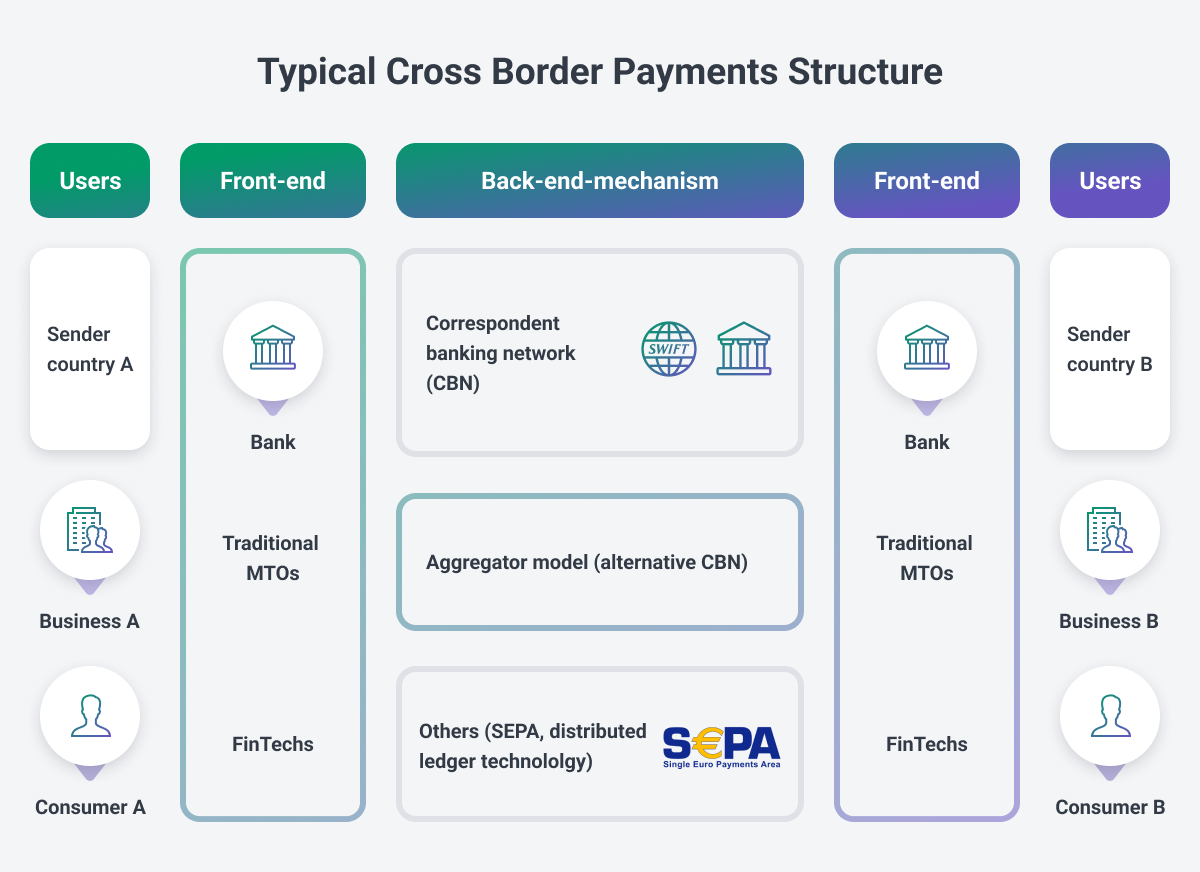

Cross-border payments involve the transfer of money between countries using methods such as bank transfers, alternative payment methods, card payments, and mobile payments. The funds undergo complex processes and approvals before reaching their intended destination and becoming available.

While cross-border payments have become more accessible for many businesses, development in this area is not evenly distributed worldwide. The report reveals that longer processing times are typically experienced in lower-income countries. For example, sending money takes an average of 12 minutes in North America, but can take up to 22 hours in South Africa.

Although payment systems may be lagging in some developing countries, the

compound annual growth rate (CAGR) of emerging markets is expected to exceed ten percent from 2018 to 2022. In comparison, developed markets are projected to grow at a CAGR of two percent during the same period. This indicates the potential for further development in emerging markets.

The Two Main Types of Cross-Border Payments

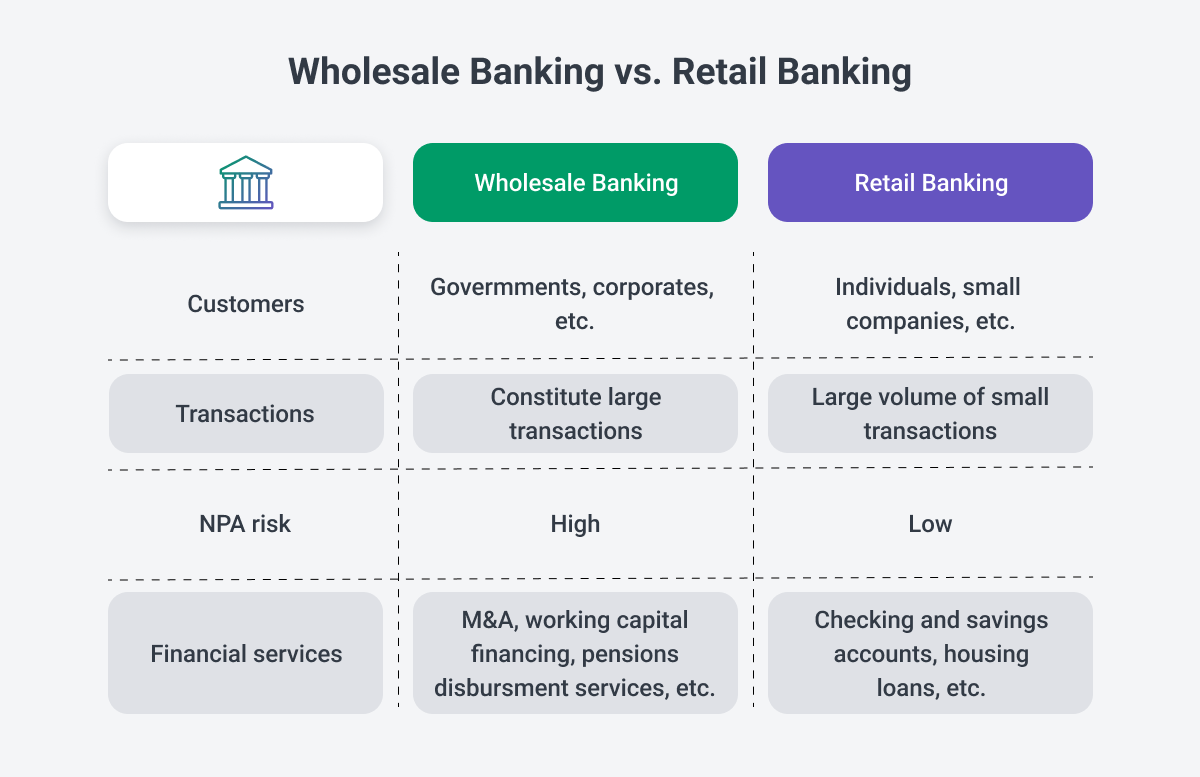

Cross-border payments can be categorized into two main types: wholesale and retail.

Wholesale cross-border payments primarily involve financial institutions and encompass activities such as lending, borrowing, debt transactions, commodities trading, and foreign exchange. Non-financial institutions and governments utilize this type of payment for large-scale imports, exports, and general trading purposes.

On the other hand, retail cross-border payments are the most prevalent in the market. They encompass transactions between individuals and businesses, including remittances and a wide range of online purchases.

What are the Innovations in Cross-Border Payments?

Businesses operating in the global market heavily rely on suppliers from different countries. To ensure smooth financial transactions, companies are urging banks to simplify and streamline international transactions. Here are two innovative solutions that exemplify progress in the industry:

APIs and real-time FX rates: APIs have gained significant attention in the banking sector. They can have a substantial impact on cross-border payments by integrating with treasury infrastructure. APIs enable access to real-time foreign exchange (FX) rates, providing better visibility for managing reconciliation processes effectively.

Virtual accounts: Virtual accounts offer clients enhanced flexibility by allowing them to manage cash flow across multiple currencies. These types of accounts empower businesses to reduce risks, increase liquidity, and utilize currencies that align with their specific business requirements. Virtual accounts provide a valuable tool for optimizing financial operations.

What Technical Problems Could be on the Horizon?

The intense competition in the fintech industry has brought forth both opportunities and challenges. Banks, neobanks, payment processors, and non-traditional financial players are introducing new solutions to facilitate smoother cross-border transactions.

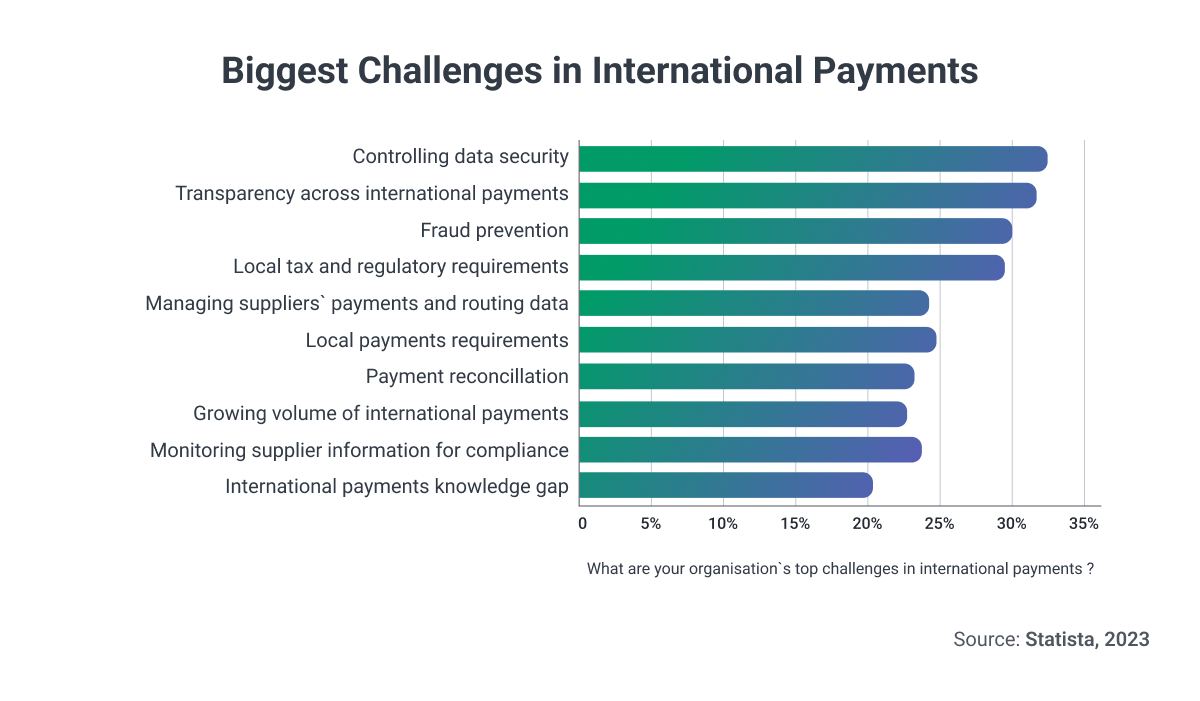

Sending money across borders presents distinct challenges, as highlighted in Endava’s 2022 Global Payments Report. The key problems include:

- Data security

- Lack of transparency in international payments

- Fraud prevention

- Complexities of local taxation

Financial institutions generally follow industry trends and are actively pursuing digitalization. However, not all players in the industry possess the same level of technological proficiency, leading to various technical issues. For instance, differing national requirements and inconsistencies in standard implementations are impeding the development of innovative cross-border payment solutions.

These are some of the prevalent problems that hinder progress in cross-border payment innovation:

1. Outdated Technology

Legacy applications lack modern cross-border payment features and functionality. For instance, they may lack real-time monitoring tools, automation, and AI/ML capabilities, resulting in slower and more cumbersome payment processes.

2. Complexity of Third-Party Providers (TPPs)

Banks often rely on third-party providers and lengthy authentication processes to facilitate money movement. Dealing with multiple parties can pose challenges and cause delays in cross-border transactions.

3. Stringent Compliance Checks

Compliance checks, while necessary, can significantly extend transaction times. The lack of consistency in processes and regulations across different countries adds friction to cross-border transactions.

4. Data Security Control

The increasing number and sophistication of cyber-attacks pose a threat to data security. Outdated legacy code and regulatory constraints hinder effective fraud protection measures. Managing cybersecurity amidst evolving regulations creates room for errors and potential fraudulent activities.

5. Automated Approvals and Fraud Detection

Automated approvals are gaining popularity in cross-border payments. However, implementing robust fraud detection tools is crucial to ensure secure transactions. These tools leverage machine learning, big data, and algorithms to verify payments and detect fraudulent activity. ML analyzes transaction data for patterns indicative of fraud, big data identifies trends for process optimization, and algorithms automate payment processing to reduce time and costs.

Despite the added security measures in automated cross-border payment systems, concerns persist about the consistent ability of fraud detection tools to identify and prevent problematic transactions.

Are Regulatory Changes Solving the Problems?

ISO 20022 – Enhancing Transactions with Consistent Data

The full adoption of ISO 20022 in 2023 holds potential for financial institutions, as it provides consistent and structured data for various transactions, including cross-border payments. This standardized information can improve the industry’s understanding of how to enhance and safeguard cross-payment systems, ensuring maximum security for users. However, successful implementation hinges on universal adoption and utilization of ISO 20022 as a common language across diverse markets.

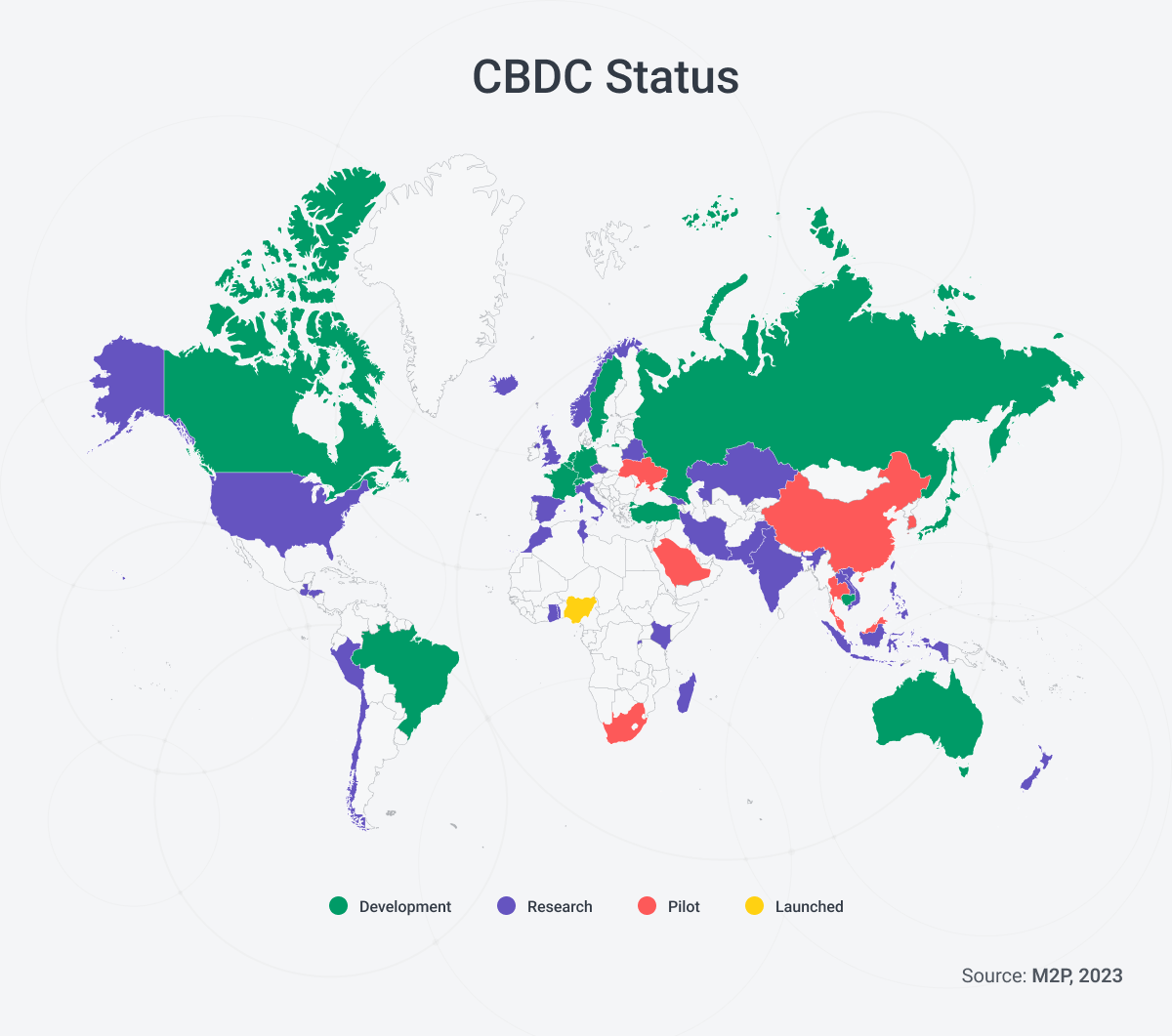

CBDC – Transforming the Industry with Central Bank Digital Currencies

Central Bank Digital Currencies (CBDCs) have emerged as potential disruptors that can facilitate faster and smoother transactions, including cross-border payments. CBDCs, available as account-based or token-based forms, act as legal tender and can be used similar to physical cash. They offer enhanced security, efficiency, and cost-effectiveness, enabling closer transaction monitoring by banks. CBDC implementation varies based on each country’s goals, whether to improve financial performance, enhance inclusion, or reduce cash usage.

Differentiating CBDCs from Cryptocurrencies

While both CBDCs and cryptocurrencies are digital currencies, they differ significantly. Cryptocurrencies are decentralized and based on blockchain technology, independent of central authorities. In contrast, CBDCs are digital versions of fiat currencies issued and backed by central banks. CBDCs provide advantages like faster transactions and lower costs compared to traditional cash. Although CBDCs are not yet mainstream for money transfers, their global popularity growth could profoundly disrupt the banking sector.

How Will Fintechs Adapt to New Realities?

Fintech companies are proactively pursuing innovation and customer-oriented features to enable faster and smoother payments. Neobanks, for instance, have obtained new licenses and built infrastructure that allows them to bypass intermediary financial institutions and offer superior services. Similarly, certain non-bank institutions possess the necessary licenses and infrastructure to facilitate direct cross-border money transfers.

Collaborating with skilled development teams, fintechs leverage distributed ledger technologies to provide enhanced transaction tracking and transparency. They can offer same-day settlements within their network of banks.

Fintechs are also adapting to stringent regulations, investing in automated compliance, algorithm-based transaction reviews, and advanced

Know Your Customer (KYC) systems. Capitalizing on the digital environment and access to cutting-edge technologies, fintechs outpace traditional banks in developing solutions for cross-border transactions.

Final Word

In the current fintech landscape, banks must prioritize innovation to maintain their competitive edge. Fintechs and neobanks have taken center stage, pushing banks into the background. To stay relevant, banks are investing significant funds in partnering with promising fintech companies that can offer advanced services and features to their customers.

The dynamics of cross-border payments are changing, necessitating a shift in how money flows across borders and continents. However, without technical expertise, meaningful transformation becomes challenging.

Therefore, banks and financial institutions must allocate resources to

enhance their IT infrastructure and engage experts who understand the latest fintech innovations. This investment is crucial for their survival in the rapidly evolving payments landscape.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: https://www.finextra.com/blogposting/24185/cross-border-payments-guide-what-can-we-expect-in-2023?utm_medium=rssfinextra&utm_source=finextrablogs